Our internal framework for identifying AI opportunities in financial services

Issue 012

Welcome back to Surfacing, Emergence Capital’s monthly newsletter. Subscribers receive the most relevant news, thoughts, trends, and jobs in the B2B SaaS ecosystem each month. Subscribe below to get the newest edition in your inbox.

🔦 FEATURED CONTENT

Framework for Founders: Where to Apply AI in Financial Services

By Lotti Siniscalco, Partner, and Kyle Murphy, Associate

Emergence’s history of investing in Industry Cloud software goes back more than 15 years. From our first investment in Veeva Systems in 2008 to Doximity in 2011 and, most recently, Federato in 2022, our original hunch holds strong: companies that go deep and focus on an industry build lasting customer loyalty.

As active investors in Industry Cloud companies, we’re always keeping a pulse on new developments in technology and how they will impact or transform the space. Today’s AI platform shift is no exception. In fact, we are thrilled about the prospects that AI holds across all Industry Cloud sectors.

We’ve seen how advancements in large language models (LLMs) have revolutionized text-based analysis, pattern recognition, and reporting. These LLMs now possess enhanced semantic understanding, allowing for these tasks to be executed more efficiently and precisely than ever before. Because analysis, synthesis, and reporting are functions that apply to all industries, we firmly believe AI will bring about radical transformations across all verticals. In this article, we’ll examine the repercussions of this transformation on the financial services industry.

Why financial services?

Financial services’ unique mix of data-driven decision-making, high-volume transactions, risk management requirements, and complex regulatory landscapes make it a compelling case study for the application of these advanced AI systems. Additionally, over the last few years, we’ve seen a sharp increase in the adoption of financial digital solutions for both consumers and businesses, as well as an explosion of availability of financial-related data.

The emergence of open banking, spearheaded by platforms like Plaid and Finicity, laid the foundation for this data revolution. We are now witnessing a further evolution of this in the “Plaid for X” model, where companies like Finch, Codat, Rutter, Merge, Pinwheel, and Argyle are enabling open data access for various financial-related sources beyond traditional banking. We believe this abundance of data, as well as the financial services industry’s increasing need for speed and personalization, will create a new generation of AI-first fintech companies that will significantly change the way the entire industry works.

However, not all subsets of the financial services industry will benefit from and embrace AI at the same rate. In the following section, we will share the framework we have developed internally to help us navigate this fast-changing environment, with the goal of understanding which pockets might be most promising for builders to focus on. We hope you’ll find it helpful.

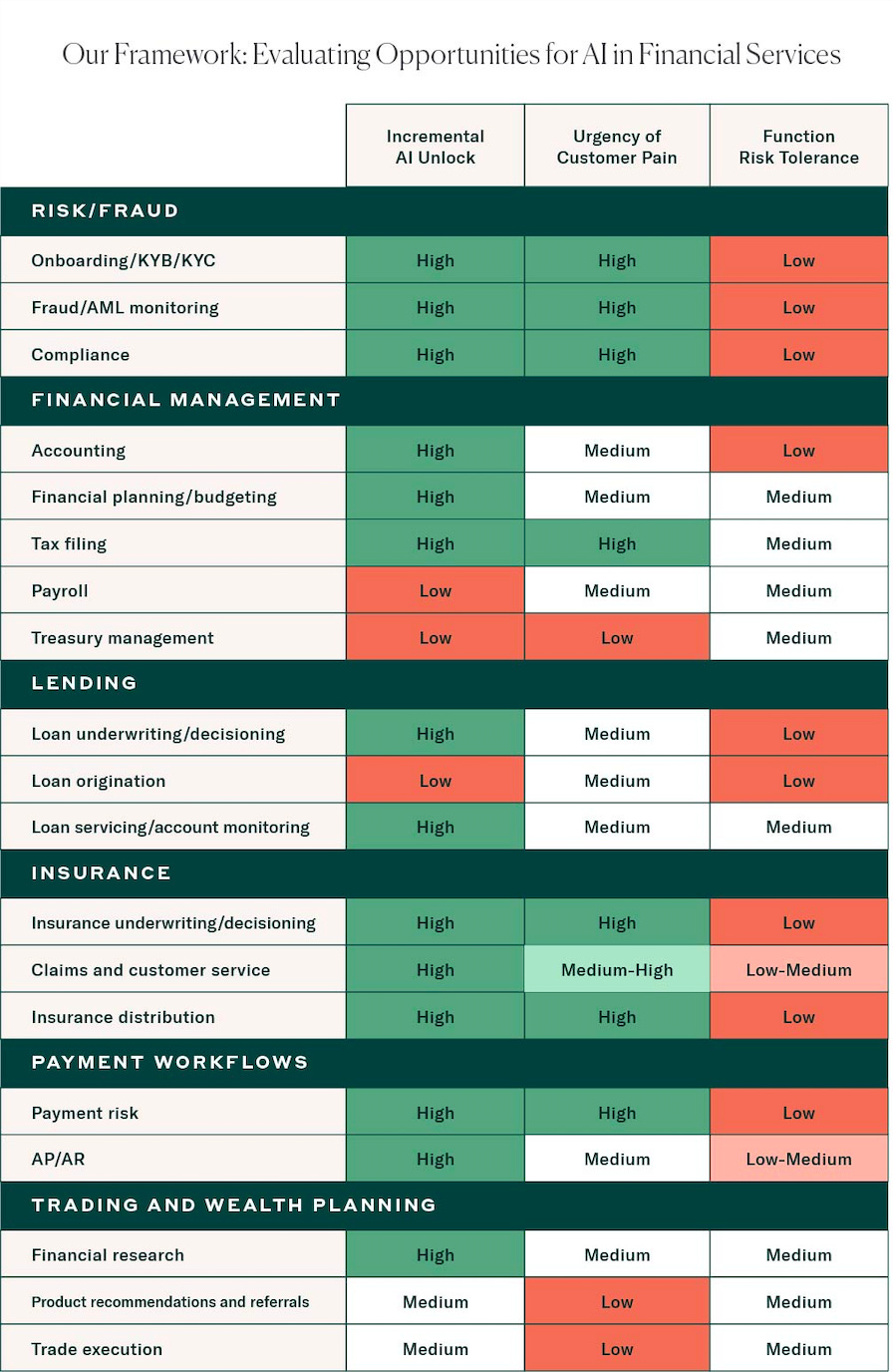

Our framework: Evaluating opportunities for AI in financial services

As a first step, we broke out the financial services industry into major categories (Financial Management, Lending, Insurance, Payments, Trading and Wealth Management, and Risk). For each, we identified the most important functions within each category (for example, within Insurance, we identified Insurance Capacity, Underwriting, Distribution, and Claims & Customer Service). We dove deep into each function, talking to users to understand their pain points, and imagined how the “job to be done” will change with AI.

After going through all functions, we ranked them based on the following three criteria:

Incremental AI Unlock. This category is meant to assess the extent to which AI can enhance existing solutions, processes, or business models. Using a first-principles approach, we considered how AI technology's ability to read or write text-based data would impact key functions, as well as its ability to find patterns, categorize, and understand large volumes of data. When doing this, we considered all aspects of the “job to be done” that could benefit from the potential AI unlock. Could AI significantly enhance the experience for the end customer? Going back to the insurance underwriting example, could an AI-powered underwriting solution help a CEO more efficiently purchase a cyber insurance policy for their company? Or how could AI improve the experience of the user within a company (in this case, the underwriter of the cyber insurance policy?) The more incremental AI unlock, the more attractive this function would be for entrepreneurs to focus on.

Urgency of Customer Pain. The more urgent the customer pain is, the more interesting the category is. While the previous criteria were focused on the technological upside that AI can provide, here we assessed the reality of the market. Existing strong and pressing customer pain is typically associated with a higher willingness to pay and shorter sales cycles, both desirable elements of a market for an entrepreneur. Here we also considered whether there are any trends supported by regulatory or technological shifts that will change the urgency of the customer pain in the near term. For example, as AI technology advances, we foresee heightened challenges in the realm of fraud prevention due to its potential misuse. We expect unscrupulous actors to leverage AI for nefarious uses, escalating the complexity and prevalence of fraudulent activities and therefore requiring more sophisticated solutions to combat it. Another example of a supporting trend, this time in payments, is FedNow, an initiative by the Federal Reserve to build a real-time payments system designed to facilitate instant monetary transactions on a 24/7 basis. As financial institutions participate in this initiative, they will have to rethink some of their tech stack to be able to process transactions instantaneously.

Function Risk Tolerance. How much risk tolerance is there within each function? Said in a different way, how high are the stakes for each function? To determine this, we considered what the implications and outcomes would be if AI were to incorrectly perform the function in our framework. For example, if the anti-money laundering (AML) function within a bank was to be incorrectly performed by AI, even just once, the implications could be catastrophic for the financial institution, as they could lose their license or be forced to pay exorbitant fines. Therefore, AML is a function with an inherently low risk tolerance. On the other hand, if AI were to incorrectly personalize a financial services offer or incorrectly answer a customer service inquiry, it would be damaging to the brand and the customer, but the risk to the company would not be existential. Therefore, distribution or customer support are functions with higher risk tolerance. We believe that everything else being equal, functions with a higher risk tolerance will likely see faster adoption of next-gen AI-powered solutions, while for lower-risk ones, buyers will want to see more proof points around models' performance and accuracy. It’s worth noting that there can be some tension between this category and the previous one: even if a function has low risk tolerance, it can still be a highly desirable place to build a company because of the massive pain points waiting to be solved. This is the case with functions such as KYC, AML, and compliance, amongst others.

Based on this framework, we identified a few areas that we think present particularly attractive near-term opportunities for founders looking to build AI-first companies. Continue reading for our analysis and reasoning.

If you’re a founder building in this space or are considering building in the space, we’d love to hear from you! Feel free to reach out to us at lotti@emcap.com and kyle@emcap.com.

📰 PRESS

Our team featured in the news

TechCrunch | TechCrunch+ roundup featuring Kevin Spain

💸 PORTFOLIO NEWS

Federato raises $25M

Congratulations to the entire Federato team on a successful Series B fundraise! Since announcing their Series A less than a year ago, Federato has tripled their customer base, doubled spend within existing customers, and entered several new segments across both commercial and personal lines.

We are thrilled to double down on our partnership and look forward to supporting the team through this next phase of growth.

🎉

🔮 PORTFOLIO JOBS

Looking for your next role?

Check out the open opportunities at our portfolio companies.

G&A and Operations

Alchemy: Legal Counsel (San Francisco)

Blend: Tax Director (Remote)

Xapo: Head of Operational Risk (Remote)

Zoom: Product Counsel (Remote)

Eng, Product & Design

Bill.com: Senior Director, Growth Data Science & Analytics (San Jose, Hybrid)

Forma: Lead Product Designer (Remote)

Project44: Head of Data Science (Chicago)

Zoom: Principal Engineer (Remote, San Jose)

GTM & Business Operations

Chorus: Director, Sales (Waltham, MA)

Doximity: VP of Strategy - Clinical Insights (San Francisco, Remote)

Federato: Head of Marketing (Remote)

Regal: Director, Product Marketing (Boston, New York, San Francisco, Hybrid)

We have ~760+ open roles on our portfolio jobs site. Check them out!